In 2020, the world witnessed a socio-economic shift as a new variant of Coronavirus (COVID-19) spread worldwide within a few weeks. The attendant death toll has crossed the 3 million across 214 countries.

The pandemic led to an erosion of human capital through job losses primarily due to lockdowns of major cities and travel restrictions. This metamorphosed into global trade fragmentation, supply linkages, and ultimately global recession. According to the World Bank, in 2020, we experienced the largest global contraction since 1870.

The case was not much different in Nigeria, although the pandemic had a lower impact than anticipated due to the absence of quality infrastructure and medical facilities. The country experienced about 167,400 cases with 2,118 deaths as a result of the microbe.

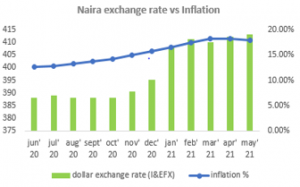

On the flip side, it has led to a significant drop in revenue, with crude oil prices tanking at below US$20/bbl in April 2020 and an average price of less than US$50/bbl for the year. The result has been a 6% drop in the country’s foreign reserves and a 27.7% drop in diaspora remittances. Accordingly, inflation rate rose from 11.98% in December 2019 to 18.12% in April 2021, and the subsequent devaluation of the Naira by over 30%.

Despite these, it was encouraging to see the Nigerian Stock Exchange ending the year as the 2nd best performing Stock Market globally.

The Federal Government, in conjunction with the Central Bank of Nigeria has had to provide various stimulus packages to several industries in an attempt to drive economic growth.

Furthermore, FG developed an Economic Growth and Recovery Plan to harmonize its strategic initiatives and has so far pledged over N3 trillion out of which over 10% is earmarked for multiple social and low-cost housing projects across the country.

These initiatives resulted in a positive Real Estate (RE) sector growth of 2.81% after 10 consecutive sectors of negative growth. In light of this, it is expected that as these initiatives are executed, they would lead to more sustainable growth in the sector.

Players in the Real Estate industry, which is highly fragmented with several small developers, have had to adapt new strategies to sell their products.

Developers, who have historically struggled to access long-term finance for project execution, have now devised ways to offer various payment plans to ease the financial burden on prospective buyers.

The RE market which is historically a seller’s market with demand outstripping supply has transformed into a buyer’s market as a growing number of medium sized firms have introduced products of various types in areas with high consumer demand.

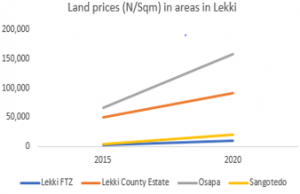

For example, the Lekki Area of Lagos which has been the fasting growing corridor in Africa for the past decade has experienced astronomical growth rates. Its proximity to Victoria Island, the Commercial Business District of the city and the expected completion of the Dangote Refinery- the largest single-train refinery in the world have made properties in the area a choice investment.

However, in the selection of properties, buyers are advised to consult experts to prevent them from making wrong investments in properties with issues like defective titles, flood-prone areas, lands under acquisition by the government. A lawyer can assist in conducting a land search at the Lands Registry of the State to confirm the property is unencumbered.

Buyers are also advised to visit a Mortgage Bank to confirm if they are eligible for a National Housing Fund (NHF) mortgage loan. The NHF loan is a government assisted mortgage facility with a maximum term of 30 years for contributors to the National Housing Fund.

The Federal Mortgage Bank of Nigeria (FMBN) offers a subsidized 6% mortgage facility with a maximum of N15 million for the building or purchase of residential accommodation.

For eligible persons, the loan approval process is usually tedious and usually takes about 12 months. However, the Federal Mortgage Bank of Nigeria has recently announced that they are planning to automate their operations to reduce the duration to about a month.

The Bank, which has disbursed about N283 billion in its 29 years of operation currently has about 5 million NHF contributors. Of these, less than 30% is made up of persons in the informal sector of the economy which is estimated to employ about 93% of the workers. The Bank plans to grow the number of NHF contributors to over 30 million by 2024 with a 50:50 ratio between the persons in formal and informal employment.

About The Author: Alpha Mead

More posts by Alpha Mead